Thursday, February 11, 2016

Further Downside Expected For Crude Oil, Ultimate Bottom At $19.80

While Oil found a near-term bottom on January 20, 2016 at $26.19 (just 33 cents off our $25.86 bottom call made on January 1, 2016), and is now approaching a retest of those levels (we are currently sitting at $26.57), we are revising our ultimate bottom call on oil to $19.80 which we believe will materialize near the end of Q1 2016 (late March). The reason for our bottom call revision is our belief that we need to see bankruptcies within the Oil Services sector before any bottom is made. Note at this time, US Oil Producers continue to pump out Oil (even at depressed spot prices) due to the fact that nearly all Oil Services names hold tremendous amount of debt relative to cash, and need to continue to produce any sort of cash flow possible to service that debt. This necessity to continue producing Oil even at very low price levels will remain an overhang on Oil prices (due to continued high supply levels amid weak demand) until cash flows weaken enough to produce bankruptcies and take production off line. Note lower US production is precisely what OPEC wants to see, and we believe this has been the primary driver of OPEC's decision to continue to keep production levels abnormally high amid weak demand. With respect to our timing call, we believe end of Q1 will mark the ultimate bottom for Oil as large institutions will look to dump everything Oil related by quarter end as they will not want clients to see heavy Oil exposure once Q1 statements are sent out. We expect this end of quarter fund divestiture will produce a capitulation type sell-off into the end of Q1 2016 with our model showing supply/demand equilibrium at $19.80. Note on the way down, there is a minor supply/demand equilibrium level at $22 which we believe will produce an oversold technical bounce to $25-26 followed by the ultimate drop below $20. Furthermore, we view any rumor of an OPEC production cut as nothing more than speculative rhetoric which we don't believe will materialize until we see sub $20 on Crude Oil.

Friday, January 1, 2016

2016 Market Prediction: FANG Trade To Unwind, Commodity Names to Become Top Performing Asset Class

As we enter 2016, we expect to see one major overlying theme to characterize the upcoming year: a significant unwinding of the long FANG/short Commodities trade. Expect to see billions in capital reallocate out of fully valued internet names FB, NFLX, AMZN, GOOG, and into undervalued (and heavily shorted) commodity names. We view the Oil Services names (OIH, DO, RIG, SLB, HAL), Steel names (X, NUE, AKS), and Fertilizer names (MOS, POT) as the biggest beneficiaries. Also expect strong performances out of small to midcap defense names on the back of strong geopolitical tension (especially within the middle east), with our favorite names being AVAV and ARTX. While we expect geopolitical tension to produce significant volatility for crude oil in early 2016, we believe Oil will produce a major generational bottom sometime during late Q1 to Q2 2016 in the $25-30 WTIC range (our model shows an exact bottom based on supply/demand equilibrium at $25.86 WTIC). We view this $25-26 level as a very strong buy and the entry point for all major Oil Services names, and moreover this level will mark the starting point of a major prolonged rally to the $60-70 WTIC level by end of 2016. In terms of acquisition plays, we view AMBA, ETSY, AVAV and DECK as names likely to be taken over in 2016. CMRX and BBRY are two other names we expect to perform very well on a percentage basis, with the former expected to move from the $7 level to $16-18, and the later to breakout to about $15-17.

2016 TOP PERFORMERS:

* USO

* OIH

* DO

* RIG

* SLB

* HAL

* BBRY

* AVAV

* ARTX

* X

* AMBA

* ETSY

* MOS

* CMRX

* DECK

2016 WORST PERFORMERS:

* FB

* AMZN

* NFLX

* GOOG

* LNKD

* DIS

2016 TOP PERFORMERS:

* USO

* OIH

* DO

* RIG

* SLB

* HAL

* BBRY

* AVAV

* ARTX

* X

* AMBA

* ETSY

* MOS

* CMRX

* DECK

2016 WORST PERFORMERS:

* FB

* AMZN

* NFLX

* GOOG

* LNKD

* DIS

Monday, January 5, 2009

"Chain of Demand" Equation For Stocks Has Broken, Market Undergoing Significant Change...

In a normal market we should've had a major countertrend rally by now. All the ingredients are there: there is a significant amount of shorts in stocks across almost every sector, bearish sentiment lies at extremes, and there is definitely capital on the sidelines. There were many days over the last couple of weeks where in a normal market we would've and should've reversed hard. However, the market has changed. What makes this market abnormal now, is the significant decline in the number of real buyers and the significant decline in buying power behind these buyers. Tons of hedge funds have fallen by the wayside and closed up shop, and those who've managed to survive are left managing much less capital. Mutual funds are being depleted by the average American pulling out cash for 2 major reasons: declining or no income and mistrust of Wall Street. Investment banks no longer exist, all are now commercial banks so they can no longer take on the same amount of risk and therefore must pare back exposure to equity markets.

The confluence of these factors is allowing shorts to essentially lean on the markets and stocks overall because they've undoubtedly recognized that longs are literally "short stacked." We've seen attempted rallies fail over and over and thats because there is no longer enough capital behind bidders to sustain large and long rallies. You need a "chain of buyers" to have long sustained "frothy" rallies....smart money + hedge funds come in first, followed by momentum traders and short covering, followed by the average joe. This equation (which I call the "The Chain of Demand") has literally disintegrated over the past several months in that the first jolt of buying pressure caused by smart money/hedge fund entry has weakened due to lower capital reserves, and the second phase of the equation, specifically the short covering aspect has been weakened due to the recognition that the first phase of the equation is weak. Meaning shorts have recognized that the institutional buying power is "short stacked" so there is now much less fear to cover because they know the smart money doesn't have enough buying power to drive and sustain long rallies. Lastly, the lack of "dumb money" or average joe money is nonexistent now as they've pulled out of the market all together. This means that the market can no longer create any frothy valuations anymore, that was the responsibility of dumb money. And again, the shorts recognize and are aware of the inability of the market to create "froth" so the fear to cover is again diminished.

Moreover, the anti-capitalist economic policy being driven by the Obama administration is adding even further disincentive for sidelined money to enter the market. What gives anyone incentive to enter the market and take on unneeded risk when the Obama administration is in the process of killing capitalism, and putting further pressure on an already weak economy through unneeded tax hikes? Believe what you will, but I'm telling you the last 2000 points of this downleg has been 100% as a result of Obama's economic policy, and the lack of buyers will continue to present itself until Obama recognizes the error of his ways. He needs to implement a policy of incentives in order to bring market participants back to the market again and take on risk. Until this happens there is no real reason to enter the market other than "stocks are cheap," and this statement lacks conviction because of the uncertainty over the cumulative long term effects of Obama's economic policy (primarily how his policy will effect overall consumer demand and corporate earnings) which ultimately leads to uncertainty over how long this downturn will truly last.

In my opinion it will take many, many years for this equation to resurrect itself again if at all. People across the entire economic spectrum are fed up with the market all together, and are in the process of saving capital rather than allocating it to high-risk investments and outright consumption of goods and services. We need to get used to and accept the fact that the market has changed and adjust ourselves to the reality of shorter rallies or a long drawn out rangebound market.

The confluence of these factors is allowing shorts to essentially lean on the markets and stocks overall because they've undoubtedly recognized that longs are literally "short stacked." We've seen attempted rallies fail over and over and thats because there is no longer enough capital behind bidders to sustain large and long rallies. You need a "chain of buyers" to have long sustained "frothy" rallies....smart money + hedge funds come in first, followed by momentum traders and short covering, followed by the average joe. This equation (which I call the "The Chain of Demand") has literally disintegrated over the past several months in that the first jolt of buying pressure caused by smart money/hedge fund entry has weakened due to lower capital reserves, and the second phase of the equation, specifically the short covering aspect has been weakened due to the recognition that the first phase of the equation is weak. Meaning shorts have recognized that the institutional buying power is "short stacked" so there is now much less fear to cover because they know the smart money doesn't have enough buying power to drive and sustain long rallies. Lastly, the lack of "dumb money" or average joe money is nonexistent now as they've pulled out of the market all together. This means that the market can no longer create any frothy valuations anymore, that was the responsibility of dumb money. And again, the shorts recognize and are aware of the inability of the market to create "froth" so the fear to cover is again diminished.

Moreover, the anti-capitalist economic policy being driven by the Obama administration is adding even further disincentive for sidelined money to enter the market. What gives anyone incentive to enter the market and take on unneeded risk when the Obama administration is in the process of killing capitalism, and putting further pressure on an already weak economy through unneeded tax hikes? Believe what you will, but I'm telling you the last 2000 points of this downleg has been 100% as a result of Obama's economic policy, and the lack of buyers will continue to present itself until Obama recognizes the error of his ways. He needs to implement a policy of incentives in order to bring market participants back to the market again and take on risk. Until this happens there is no real reason to enter the market other than "stocks are cheap," and this statement lacks conviction because of the uncertainty over the cumulative long term effects of Obama's economic policy (primarily how his policy will effect overall consumer demand and corporate earnings) which ultimately leads to uncertainty over how long this downturn will truly last.

In my opinion it will take many, many years for this equation to resurrect itself again if at all. People across the entire economic spectrum are fed up with the market all together, and are in the process of saving capital rather than allocating it to high-risk investments and outright consumption of goods and services. We need to get used to and accept the fact that the market has changed and adjust ourselves to the reality of shorter rallies or a long drawn out rangebound market.

Monday, September 15, 2008

Equity Market Being Used As Source Of Funds By Financial Institutions...

The stock market is being used as a source of funds right now which is not good....the largest players in the equity market have major major capital issues right now....AIG needs $80 Billion just to survive, that is a HUGE number (Goldmans entire market cap is $53B...they basically need a Goldman and a half) and they are just one major player....sure, institutions and market participants across the financial spectrum have used the equity market as a source of funds for a long time but never have the largest institutions in the financial ecosystem been under this much pressure to raise capital...and never have they experienced the need to raise capital for the ultimate sake of survival...that need to raise capital to meet margin calls in order to survive was usually (for the most part) limited to us the small guy...the market could easily weather that kind of selling pressure as long as the big guys were in there buying our stock on the cheap as we forcibly liquidated our holdings...now the shoe's on the other foot with large institutions joining us aggressively on the ask, which puts us in uncharted waters....liquidation of this magnitude leads to extremely rapid declines in asset prices especially those assets widely held by many large institutions....this rapid deterioration in stock prices ultimately leads to the point where stocks are no longer viewed as representing ownership in fundamentally sound companies but rather as a mere source of funds...a way to raise cash....you sell stock you get cash, thats what institutions need cash.....this is when panic begins to set in, it gets scary and stock markets crash, its when people become fearful of owning stocks as an asset class because of rapidly declining asset prices. after todays action you can tell real fear is developing in the market and people are really JUST starting to get a bit nervous about owning stocks....you're starting to see stocks that were worth $60-70/share go to zero....and these arent just any stocks, they were the biggest balls in the market....people are starting to think about what they own and what its really worth if panic sets in....i mean is it that far fetched to see AAPL selling in the 90s....the big boys could sell that stock off another 40 points down to $100 and funds would still be getting out with a profit...thats how you have to think right now....think about how much fund ownership your stocks have and know that those funds are having major problems and need cash.

Monday, July 14, 2008

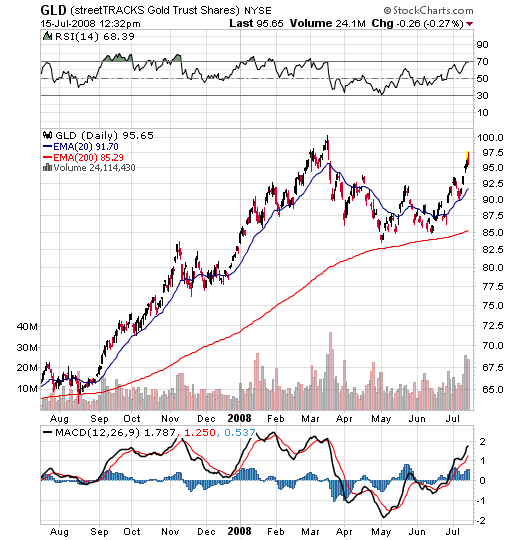

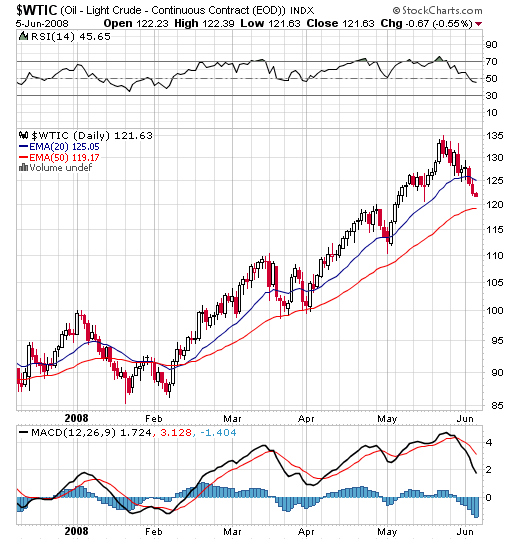

Gold To Replicate Oils Parabolic Move, 30-Year Treasury Yields To Soar...

With multiple bank failures looming and the US government doing nothing but take on bad debt and assets onto their balance sheet we are looking for new lows in the US dollar as the fundamental backdrop of the US financial system continues to worsen by the day. Inflationary pressures continue to mount with Oil and food hovering near their all-time highs, and the US continues to be hardest hit with respect to inflation due to the high cost of imports based on the declining purchasing power of the dollar. Note that while Europe for example has to pay the same $145 for a barrel of Oil that we do, their currency has also appreciated almost 20% since last year thereby mitigating some of their inflationary pressure. Furthermore, with the US posting its sixth straight month of job losses in June, and the employment picture getting seemingly worse by the day, you can expect the unemployment rate to start ticking up toward 6% by year end. Take into consideration that these looming bank failures will definitely lead to large job losses in financial services in addition to layoffs recently announced within the energy-sensitive transportation sector i.e. airlines and car companies like GM.

In essence, what is happening is that the US government is taking on very large amounts of debt at the same time that their revenue base (i.e. tax collection) is declining due to higher unemployment and high inflation which curbs consumer spending on discretionary items and hence produces slower growth for US corporations and therefore less corporate tax generation. Think of the US as a large company with debt levels climbing significantly and revenue and profit declining. What usually happens in a situation like this? Well lenders usually begin to become much less willing to lend capital at prevailing rates, and at the same time the debt-laden institution is more likely to want to raise additional capital to maintain sufficient debt to equity ratios (and/or bailout failing financial institutions). The rising debt levels coupled with declining income lead to the perception of a higher probability of default (even if slightly) and the higher probability gets priced into borrowing costs in the form of higher rates needing to be paid to lenders. What will happen is that demand for newly issued treasuries will begin to wane and large current holders of bonds (ie China and Japan) will likely be more inclined to reduce their holdings of US debt as risk levels associated with these bonds rise in conjunction with the fact that the value of these bonds continue to decline due to the devaluation of the dollar. You can see how a situation like this turns into a rather vicious circle, with weak fundamentals affecting dollar values and dollar values causing a negative change in behavior which in turn puts pressure on fundamentals. High inflation coupled with slow growth, rising unemployment, a weak currency, and rising debt levels is likely the worst situation an economy can be in which is why monetary policy is seen as so critical in maintaing all-important price stability. When inflation begins to soar, and central banks begin to lose credibility in containing inflation expectations it is very difficult to work an economy back to stable ground without severe consequences. Hence, we are expecting the yield on the 30-Year Treasury Bond to go much higher than the 4.44% it currently sits at as the risk associated with holding US debt increases and the expectation of prolonged high inflation begins to take form. Note that while the Fed has full control over rates at the short end of the yield curve (ie Fed Funds Rate), the Fed has zero control over yields at the long end which are completely set by open market forces.

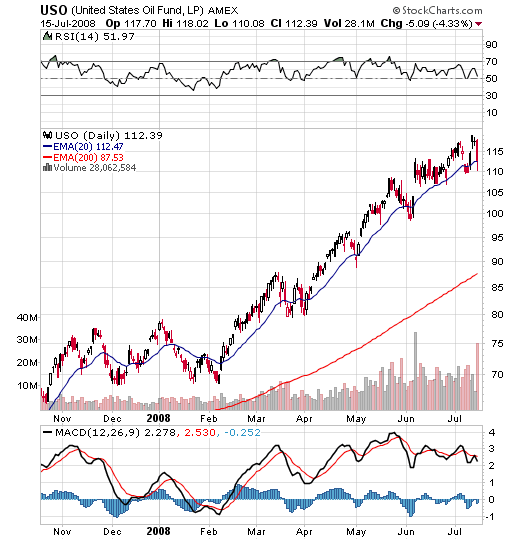

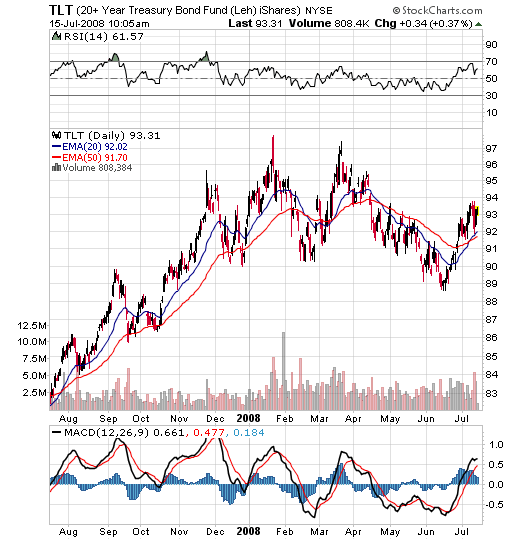

Now looking at the trades, Gold has several things going for it on a fundamental as well as technical basis. First off, we are in a financial storm predicated on worries over the soundness of financial institutions and the inherent value of the US dollar. This is the perfect backdrop for gold, as global investors tend to run to the yellow metal as the ultimate safe haven in times of uncertainty within the financial system. Secondly, inflation expectations remain high and the dollar continues to weaken. Thirdly, central bank diversification out of US bonds is likely to benefit gold as central banks tend to increase their gold holdings in times of uncertainty and environments where risk aversion is prevalent. Fourthly, the recent double bottom at 85 on the GLD chart looks eerily similar to the double bottom at 80 we spotted on the USO chart back in March which ultimately presaged Oils parabolic move from the 80s to 140s. Take a close look at the USO chart below, paying particular attention to the mid March 2008 to early April 2008 double bottom at 80. Now stretch it out over a couple months rather than one month, and notice how closely it resembles the mid April to mid June double bottom at 85 on the GLD chart. They are almost perfect replicas and we believe we are at the same exact stage of the Gold breakout with respect to Oil....just beginning a major move to the upside. Moreover, with Oil nearly doubling over the past year and significant percentage gains made, it is likely that hedge funds and large institutions are now in search of the next asset class which may have greater potential for larger percentage gains down the road. This will likely lead them to Gold, as the asset class is similar and it keeps them highly hedged against inflation. Hence, with fundamentals as well as technicals in place we believe that Gold has potential to become the new Oil going into year end, and are looking for a very strong double top breakout over 100 in the GLD very soon. In this kind of environment, with inflation expectations running high as well as multiple looming bank failures there really is no limit to how high Gold can go. Would it surprise me to see $1500-2000/oz by year end? No. Based on these assumptions, we have been buying the September 100 GLD calls here and will likely sit on these until Gold breaks out over $1000. Also note that large institutions have been taking extremely large positions in these calls over the past few sessions, with over 60,000 calls being bought yesterday and over 110,000 in open interest. Second of all, we have also been buying the September 90 puts on the TLT which is iShares Lehman 20+ Year Treasury Bond ETF. It essentially tracks bond prices at the long end of the yield curve, and since we are bearish on bonds going forward we'd like to have some exposure to the downside move.

Now looking at the trades, Gold has several things going for it on a fundamental as well as technical basis. First off, we are in a financial storm predicated on worries over the soundness of financial institutions and the inherent value of the US dollar. This is the perfect backdrop for gold, as global investors tend to run to the yellow metal as the ultimate safe haven in times of uncertainty within the financial system. Secondly, inflation expectations remain high and the dollar continues to weaken. Thirdly, central bank diversification out of US bonds is likely to benefit gold as central banks tend to increase their gold holdings in times of uncertainty and environments where risk aversion is prevalent. Fourthly, the recent double bottom at 85 on the GLD chart looks eerily similar to the double bottom at 80 we spotted on the USO chart back in March which ultimately presaged Oils parabolic move from the 80s to 140s. Take a close look at the USO chart below, paying particular attention to the mid March 2008 to early April 2008 double bottom at 80. Now stretch it out over a couple months rather than one month, and notice how closely it resembles the mid April to mid June double bottom at 85 on the GLD chart. They are almost perfect replicas and we believe we are at the same exact stage of the Gold breakout with respect to Oil....just beginning a major move to the upside. Moreover, with Oil nearly doubling over the past year and significant percentage gains made, it is likely that hedge funds and large institutions are now in search of the next asset class which may have greater potential for larger percentage gains down the road. This will likely lead them to Gold, as the asset class is similar and it keeps them highly hedged against inflation. Hence, with fundamentals as well as technicals in place we believe that Gold has potential to become the new Oil going into year end, and are looking for a very strong double top breakout over 100 in the GLD very soon. In this kind of environment, with inflation expectations running high as well as multiple looming bank failures there really is no limit to how high Gold can go. Would it surprise me to see $1500-2000/oz by year end? No. Based on these assumptions, we have been buying the September 100 GLD calls here and will likely sit on these until Gold breaks out over $1000. Also note that large institutions have been taking extremely large positions in these calls over the past few sessions, with over 60,000 calls being bought yesterday and over 110,000 in open interest. Second of all, we have also been buying the September 90 puts on the TLT which is iShares Lehman 20+ Year Treasury Bond ETF. It essentially tracks bond prices at the long end of the yield curve, and since we are bearish on bonds going forward we'd like to have some exposure to the downside move.

Friday, July 11, 2008

REPOST: Global Darwinian Forces May Produce Major Exogenous Event Blindsiding US Economy...

We wrote this article back on April 5th, and think it is extremely relevant to our current global situation, all comments welcome:

By all economic measures, the United States is clearly in a state of marked weakness. Economic growth is at or near zero, unemployment is rising, the banking system is in critical condition, housing prices continue to decline, the US consumer is up to its ears in debt, the dollar continues to make new lows versus every major currency, inflation shows no signs of abating, and the Fed is running around like a headless chicken literally doing everything it can to prevent the entire system from collapsing. This is not a subjective assessment, it is our grave reality. So what now? Where do we go from here?

Well the obvious answer would be to fix everything that appears to be broken, clean up inefficient systems, attempt to reinvigorate the economy, and ultimately rebuild confidence in the US financial system over time. However, what I fear most is that in this time of distress we may no longer have the luxury of time. I believe it is possible that one of the many emerging superpowers may make a play for global dominance in the near future. Yes, I know this is a bold statement, but let me explain. Over the past several decades the United States has clearly been the world's superpower. It has been the steam engine driving the global economy as continuous wealth creation here has driven demand for foreign goods thereby creating wealth and GDP growth overseas. We are clearly the largest consuming nation in the world, and most of our foreign counterparties have done everything they can to see that growth here continues as incremental gains in US GDP inevitably trickle down to their own economies. However, it appears now that the global economy has approached the point where our significance in the global growth equation has diminished. It appears as if our emerging market counterparties have grown to a level where collectively they are able to maintain global growth without the neccessity of US demand. Where is the evidence of this? The commodities market. We have virtually every major commodity (Gold, Oil, Coal, Grains, Corn) at or near nominal highs, with many now approaching their inflation-adjusted highs. What is most notable however is that these commodities are making this move with the United States literally on the brink of recession! How is this possible? How is it possible that Oil is near $110 per barrel with such weak US demand? How is it possible with the US near recession that global Oil demand is still greater than global Oil supply with Oil being pumped at maximum capacity? It is because of decoupling. The world no longer relies on the US as the primary engine of global growth anymore. This position has been taken over by the likes of China, India, and Brazil. While the US has been toiling with credit crises, a housing slump, and increasing debt loads, the emerging economies have grown into such a dominant state of hypergrowth that their only challenge is to make sure that growth does not get so excessive that it becomes unsustainable, and moreover that inflation remains contained. This dominant position, I'm afraid, may produce some sort of climactic consequence for the United States. Let me explain.

We as mere individuals, will never understand the desire to become a global superpower. This desire is something reserved for continents, nations, and unions as it is impossible for us as mere individuals to achieve such status. However, even though we may not have the capacity to understand this desire, we know that it exists. We know that every single day every sovereign nation is actively working or has the innate desire to become the strongest entity in the world. Why does this happen? What is the driving force behind this phenomenon? Well in my opinion it is driven by the underlying principle that the world lacks enough supply of natural resources to prolong the existence of every single nation over the long run. Over time, as the world begins to approach levels where natural resources are being fiercely competed over because of inadequate supplies and/or unusually high global demand at the margin, the strongest nations will attempt to force weaker nations into further weakness in the hope that this action may curtail overall demand and allow the strongest nations to accumulate necessary supplies at cheaper prices. It is Darwinism at its purest, and it is ultimately driven by the idea that while economic harmony may exist when the strongest parties are satisfied with the distribution of goods and resources, extreme competitive behavior will arise when those parties become dissatisfied with the allocation of resources, especially those resources necessary for independent survival. It is very much akin to the behavior of animals living in a jungle free from the so-called orders of society. When all animals including the strongest are fed and all so-called entities appear satisfied, harmony may exist because there is no need for competition as supplies of resources are adequate enough to meet the demands of all entities. However, if/when the strongest entities become dissatisfied with their levels of consumption, we will likely see an extreme uptick in competitive behavior as the idea of the natural order for satisfaction dictates that the strongest must be first to be completely satisfied. If/when this natural order appears to be imbalanced in that the strongest are not receiving adequate supplies, the strongest entities will likely seek to not only eliminate those entities which they believe will restore natural balance, but they will specifically seek to eliminate those who they believe will be easiest to eliminate (i.e. those entities who appear weakest). Make sense? Ok so what resource are we speaking of specifically when we speak of resources necessary for survival? We are speaking of crude Oil. Every single other commodity is secondary to crude oil in terms of necessity for survival. Gold, corn, wheat, coal, even steel are all secondary commodities. We don't need corn or even grain to survive, and coal and other fossil fuels are simply alternatives to the most important fossil fuel of all, crude oil. Without crude oil, factories would come to a stand still, refineries would be unable to produce gasoline, airplanes would be grounded, heating oil would be unable to be produced, and ultimately unemployment would skyrocket as productive inputs are unable to function and means of transportation become idle. It is the reason why there is literally no limit to how high the price of oil can go over the long run. Its significance as the world's primary energy source produces wars, wreaks havoc within the economic supply chain, and has the capacity to bring entire nations to its knees.

By all economic measures, the United States is clearly in a state of marked weakness. Economic growth is at or near zero, unemployment is rising, the banking system is in critical condition, housing prices continue to decline, the US consumer is up to its ears in debt, the dollar continues to make new lows versus every major currency, inflation shows no signs of abating, and the Fed is running around like a headless chicken literally doing everything it can to prevent the entire system from collapsing. This is not a subjective assessment, it is our grave reality. So what now? Where do we go from here?

Well the obvious answer would be to fix everything that appears to be broken, clean up inefficient systems, attempt to reinvigorate the economy, and ultimately rebuild confidence in the US financial system over time. However, what I fear most is that in this time of distress we may no longer have the luxury of time. I believe it is possible that one of the many emerging superpowers may make a play for global dominance in the near future. Yes, I know this is a bold statement, but let me explain. Over the past several decades the United States has clearly been the world's superpower. It has been the steam engine driving the global economy as continuous wealth creation here has driven demand for foreign goods thereby creating wealth and GDP growth overseas. We are clearly the largest consuming nation in the world, and most of our foreign counterparties have done everything they can to see that growth here continues as incremental gains in US GDP inevitably trickle down to their own economies. However, it appears now that the global economy has approached the point where our significance in the global growth equation has diminished. It appears as if our emerging market counterparties have grown to a level where collectively they are able to maintain global growth without the neccessity of US demand. Where is the evidence of this? The commodities market. We have virtually every major commodity (Gold, Oil, Coal, Grains, Corn) at or near nominal highs, with many now approaching their inflation-adjusted highs. What is most notable however is that these commodities are making this move with the United States literally on the brink of recession! How is this possible? How is it possible that Oil is near $110 per barrel with such weak US demand? How is it possible with the US near recession that global Oil demand is still greater than global Oil supply with Oil being pumped at maximum capacity? It is because of decoupling. The world no longer relies on the US as the primary engine of global growth anymore. This position has been taken over by the likes of China, India, and Brazil. While the US has been toiling with credit crises, a housing slump, and increasing debt loads, the emerging economies have grown into such a dominant state of hypergrowth that their only challenge is to make sure that growth does not get so excessive that it becomes unsustainable, and moreover that inflation remains contained. This dominant position, I'm afraid, may produce some sort of climactic consequence for the United States. Let me explain.

We as mere individuals, will never understand the desire to become a global superpower. This desire is something reserved for continents, nations, and unions as it is impossible for us as mere individuals to achieve such status. However, even though we may not have the capacity to understand this desire, we know that it exists. We know that every single day every sovereign nation is actively working or has the innate desire to become the strongest entity in the world. Why does this happen? What is the driving force behind this phenomenon? Well in my opinion it is driven by the underlying principle that the world lacks enough supply of natural resources to prolong the existence of every single nation over the long run. Over time, as the world begins to approach levels where natural resources are being fiercely competed over because of inadequate supplies and/or unusually high global demand at the margin, the strongest nations will attempt to force weaker nations into further weakness in the hope that this action may curtail overall demand and allow the strongest nations to accumulate necessary supplies at cheaper prices. It is Darwinism at its purest, and it is ultimately driven by the idea that while economic harmony may exist when the strongest parties are satisfied with the distribution of goods and resources, extreme competitive behavior will arise when those parties become dissatisfied with the allocation of resources, especially those resources necessary for independent survival. It is very much akin to the behavior of animals living in a jungle free from the so-called orders of society. When all animals including the strongest are fed and all so-called entities appear satisfied, harmony may exist because there is no need for competition as supplies of resources are adequate enough to meet the demands of all entities. However, if/when the strongest entities become dissatisfied with their levels of consumption, we will likely see an extreme uptick in competitive behavior as the idea of the natural order for satisfaction dictates that the strongest must be first to be completely satisfied. If/when this natural order appears to be imbalanced in that the strongest are not receiving adequate supplies, the strongest entities will likely seek to not only eliminate those entities which they believe will restore natural balance, but they will specifically seek to eliminate those who they believe will be easiest to eliminate (i.e. those entities who appear weakest). Make sense? Ok so what resource are we speaking of specifically when we speak of resources necessary for survival? We are speaking of crude Oil. Every single other commodity is secondary to crude oil in terms of necessity for survival. Gold, corn, wheat, coal, even steel are all secondary commodities. We don't need corn or even grain to survive, and coal and other fossil fuels are simply alternatives to the most important fossil fuel of all, crude oil. Without crude oil, factories would come to a stand still, refineries would be unable to produce gasoline, airplanes would be grounded, heating oil would be unable to be produced, and ultimately unemployment would skyrocket as productive inputs are unable to function and means of transportation become idle. It is the reason why there is literally no limit to how high the price of oil can go over the long run. Its significance as the world's primary energy source produces wars, wreaks havoc within the economic supply chain, and has the capacity to bring entire nations to its knees.

Monday, July 7, 2008

US Economy At Major Turning Point, Intervention Needed Now...

Paulson + Bernanke & Co. have been awfully quiet while we sit here at this critical juncture in the economy and markets, and they really need to step in and do something now if they plan on averting a major economic meltdown. This malaise we currently sit in is at a major pivot point in my opinion. Once Oil breaks above $150 and the DOW breaks down into the 10,000 range it's over, as confidence will have been completely shot and any sort of intervention will have minimal impact. Whether its forex intervention, raising interest rates, and/or raising margin requirements it needs to be done now. Say what you want, but a combination or dollar intervention + raising margin requirements should take some wind out of the sails of Oil and a host of other commodities. Yes I know, Oil is a supply/demand story but breaking the momentum might buy some time for the reality of a global slowdown to set in. Second of all, we are nearing the start of the all important China Olympics which have been an important contributor to demand for energy as China gears up to showcase its country to the entire world. After the culmination of the Olympics or likely before that (as the mkt is forward looking) we should see commodity prices start to come down as the market begins to price in slower economic growth out of China. The rebuilding efforts due to the devastating earthquake in China is sort of a wild card, but the way I see it, it ends up being a zero sum contributor as the increase in government spending to rebuild the country will likely get cancelled out by a decrease in consumer demand due to the necessity of millions of people needing to rebuild their lives first and foremost. Thirdly, the slowdown which appears to be picking up steam overseas in europe is likely a net positive for the US as the relative weakness associated with the dollar and the US economy dissipates a bit as market participants begin to realize that the US is not much worse off than our european counterparts, and may in fact be closer to the end of their malaise than those just beginning to slowdown. We are in such a complex economic environment with Oil + food making all time nominal highs, inflation fears accelerating, slowdowns picking up overseas, the continued perceptions of stress within the banking system, and housing prices continuing to decline that something needs to happen now at least as an effort to quell the momentum to the downside. Traditional, untraditional, it doesn't matter, time is really against us at this point as every day that goes by things seem to get a bit worse. What the puppet masters behind the curtain are doing right now is beyond me, but i have a feeling they're working on something....just doesnt make sense that theyre just waiting for this thing to play out as they know what the end result is if nothing is done.

Friday, June 27, 2008

Multilateral US Dollar Intervention Likely On The Horizon...

With the Fed's credibility waning, market technicals broken, commodities on the verge of major breakouts, and the US Dollar within striking distance of new lows we believe we are now in the red zone for an aggressive move by the US government to intervene in the foreign exchange market and stem the slide in the US dollar. The dollar slide has undoubtedly been the culprit for much of the markets malaise, as its relentless decline has put significant upside pressure on commodities pushing oil and gasoline to all time highs. With the Fed unable to adjust monetary policy favoring a strong dollar (i.e. higher rates) for fear of adding further strains on an already cash-strapped consumer, we are looking for the US government to step in and use the untraditional measure of intervention within the foreign exchange market in an attempt to not only break the back of a raging bull market in commodities, but more importantly regain global confidence in the greenback and the US financial system. We are looking for the US government to step in multilaterally, joining hands with their european counterparts as europeans also view the soaring euro as an unwelcome hinderance to domestic growth due to the fact that it makes their goods more expensive to foreign buyers and thereby makes them less competitive in the global marketplace. We are looking for possible intervention this sunday night or next week, and as such have taken a long position in the July 115 DIA calls here at $1.76 as the DOW is now firmly in oversold territory, and either way a bounce is very likely next week.

Monday, June 23, 2008

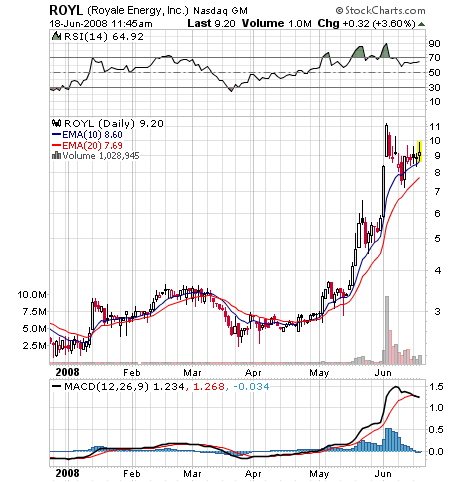

Royale Energy (ROYL) Strikes Oil, Stock Set To Go Parabolic...

As we've mentioned many times over the past several weeks, we have been aggressive buyers of ROYL on every dip, and with the company putting out an operational update minutes ago we couldn't be more excited about the prospects of the company, and feel very strongly that the stock is setting up for a parabolic move to the upside here a la PDO as in addition to extremely bullish findings of natural gas in their Uintah Basin acreage, they have also discovered what might possibly be a huge pool of oil.

Here are some excerpts specifically regarding the addition of oil to Royale's growing asset base:

"In addition, the Company believes the shallow Castlegate formation that is part of the Mesa Verde group of sands is shown on the logs to be present in two of the Company’s wells and covers a large area. This formation has shown both natural gas in the most updip location, as well as tar in the structurally lower position. If productive, this zone could result in production of both natural gas and oil from an area of almost three miles of structural dip."

"In California’s San Joaquin Basin, Kern County, Royale intends to drill an additional penetration of the Monterey oil shale. After analyzing the results of its last completion (Weber 27x-27) the Company will follow completion procedures that were developed in its latest test that resulted in the Monterey formation free flowing to the surface without pumping. Royale believes this to be extremely significant considering all of the Company’s previous perforations of the Monterey shale never achieved this. In addition, the oil cut has increased substantially over previous tests."

We did not expect these new oil finds and view this as an extremely bullish finding as we expect them to use a parallel strategy to their natural gas production of selling the Oil on a completely unhedged basis. In addition, the CEO stated that Royale has returned back to profitability this quarter and are looking for continued profitability for the foreseeable future, which is also excellent news. We are upping our initial target from the $15-20 range to $20-25 based on our belief that Royale's current $80M market cap does not accurately reflect the company's growing asset base and 100% unhedged natural gas production. As such we continue to hold ROYL as our top pick in the energy space.

Here are some excerpts specifically regarding the addition of oil to Royale's growing asset base:

"In addition, the Company believes the shallow Castlegate formation that is part of the Mesa Verde group of sands is shown on the logs to be present in two of the Company’s wells and covers a large area. This formation has shown both natural gas in the most updip location, as well as tar in the structurally lower position. If productive, this zone could result in production of both natural gas and oil from an area of almost three miles of structural dip."

"In California’s San Joaquin Basin, Kern County, Royale intends to drill an additional penetration of the Monterey oil shale. After analyzing the results of its last completion (Weber 27x-27) the Company will follow completion procedures that were developed in its latest test that resulted in the Monterey formation free flowing to the surface without pumping. Royale believes this to be extremely significant considering all of the Company’s previous perforations of the Monterey shale never achieved this. In addition, the oil cut has increased substantially over previous tests."

We did not expect these new oil finds and view this as an extremely bullish finding as we expect them to use a parallel strategy to their natural gas production of selling the Oil on a completely unhedged basis. In addition, the CEO stated that Royale has returned back to profitability this quarter and are looking for continued profitability for the foreseeable future, which is also excellent news. We are upping our initial target from the $15-20 range to $20-25 based on our belief that Royale's current $80M market cap does not accurately reflect the company's growing asset base and 100% unhedged natural gas production. As such we continue to hold ROYL as our top pick in the energy space.

Wednesday, June 18, 2008

Sell Half PDO FPP Shares, Let The Rest Ride As Oil Set To Make New Highs...

We have taken half of our positions off PDO and FPP at $29.50 and $7 respectively and are letting the rest of our shares ride. While we believe both stocks are headed higher on fresh highs in crude Oil, we must be prudent in taking some profits off the table after a 58% run in PDO shares from our $18.60-$18.70 entry and a 38% run in FPP shares from our $5.02-$5.07 entry taken 2 weeks ago (see our June 5th blog post). With the July contract in crude expiring this friday we expect Oil to be highly attracted to the $140 level as hedge funds clearly continue to be net long Oil and have an interest in closing Oil strong into expiration. As such we continue to hold half our PDO and FPP positions as well as 100% of our ROYL position as we believe energy prices will continue to be elevated with pressure to the upside. Natural gas continues to be our favorite sector in the market right now as we believe the $15-17 level in spot prices is inevitable, and we therefore continue to be huge holders of ROYL as the company remains completely unhedged and continues to increase natural gas production.

Royale Energy (ROYL) Preparing For High Volume Breakout To New Highs...

We have added to our ROYL position here at $9.26 as the stock looks prepped for a high volume breakout to the upside today or tomorrow. Note that ROYL is flagging exactly as it did in the $5s just before it broke out to the $11s. We are looking for a similar breakout here to new highs +$11.30 shortly. Note that nat gas prices are showing remarkable relative strength versus crude, with nat gas continuing to make new highs even in the face of any short term weakness in crude.

Monday, June 16, 2008

SatCon (SATC) In Bed With Google...

It appears SatCon is also in bed with Google:

SatCon was key in Google's solar farm

Published: June 27, 2007 at 2:36 PM

BOSTON, June 27 (UPI) -- Boston's SatCon Technology Corp. had a hand in the recent installation of one of the world's largest solar arrays.

The solar farm at Google's corporate headquarters in Mountain View, Calif., was in part due to Boston-based SatCon Technology's PowerGate inverters.

SatCon is a developer of power management and system architecture solutions for the alternative energy and distributed power markets.

The company's PowerGate commercial grade inverters were an integral part of the recent installation at Google's Mountain View campus. Google officials say the new 1.6 megawatt system is the largest commercial photovoltaic system in the United States.

Sharp Corp. provided 9,212 208-watt modules for the project, which was designed and installed by EI Solutions. SatCon's PowerGate high-efficiency inverters are a critical component of the system, converting the sun's energy produced by the photovoltaic panels into alternating current electricity that is used to power the facility.

Officials estimate Google's new solar array could prevent as much as 3,637,627 pounds per year of harmful greenhouse gases annually. Over the next 30 years, the carbon dioxide reduction will be equivalent to eliminating more than 128 million car driving miles.

SatCon's trademarked PowerGate inverters are designed for use with alternative energy power systems to generate distributed electrical power. Distributed, alternative energy power generation is a growing trend toward the production of clean, reliable power at the point of use. Alternative energy systems can alleviate congestion on highly loaded utility electrical distribution networks and offer an alternative to power line extensions in remote areas.

© 2007 United Press International. All Rights Reserved.

This material may not be reproduced, redistributed, or manipulated in any form.

SatCon was key in Google's solar farm

Published: June 27, 2007 at 2:36 PM

BOSTON, June 27 (UPI) -- Boston's SatCon Technology Corp. had a hand in the recent installation of one of the world's largest solar arrays.

The solar farm at Google's corporate headquarters in Mountain View, Calif., was in part due to Boston-based SatCon Technology's PowerGate inverters.

SatCon is a developer of power management and system architecture solutions for the alternative energy and distributed power markets.

The company's PowerGate commercial grade inverters were an integral part of the recent installation at Google's Mountain View campus. Google officials say the new 1.6 megawatt system is the largest commercial photovoltaic system in the United States.

Sharp Corp. provided 9,212 208-watt modules for the project, which was designed and installed by EI Solutions. SatCon's PowerGate high-efficiency inverters are a critical component of the system, converting the sun's energy produced by the photovoltaic panels into alternating current electricity that is used to power the facility.

Officials estimate Google's new solar array could prevent as much as 3,637,627 pounds per year of harmful greenhouse gases annually. Over the next 30 years, the carbon dioxide reduction will be equivalent to eliminating more than 128 million car driving miles.

SatCon's trademarked PowerGate inverters are designed for use with alternative energy power systems to generate distributed electrical power. Distributed, alternative energy power generation is a growing trend toward the production of clean, reliable power at the point of use. Alternative energy systems can alleviate congestion on highly loaded utility electrical distribution networks and offer an alternative to power line extensions in remote areas.

© 2007 United Press International. All Rights Reserved.

This material may not be reproduced, redistributed, or manipulated in any form.

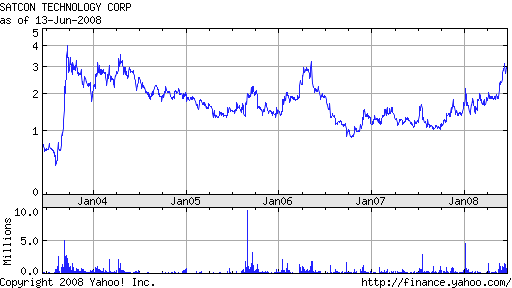

Buy SatCon Tech (SATC) As Stock Set For Major Breakout...

We are buying SATC here under $3.10 as we believe the stock is setting up for a major breakout above its May 2006 high at $3.30 taking it to its September 2003 high of $4.30 near term. If the stock can breach the $4.30 level the sky is the limit as there is no resistance in the area just above it. The company provides energy conversion technology to the alternative energy space and has shown extremely strong year over year revenue growth of 79% with growth across all major product lines. This stock reminds us of a baby Energy Conversion Devices (ENER) and with that stock making new highs today, we expect the market to sit up and take notice of SATCs similar business line leading to a strong move in the stock. Initial target $4.30, with upside to $10 should we breach the September highs.

Wednesday, June 11, 2008

Reinitiate Position In Royale Energy (ROYL) Here @ $7.40...

We believe the stock has bottomed here, and are looking for the next upleg to begin today or tomorrow. Natural gas prices remain firm with a strong bias to the upside. We also have a $4M round of financing out of the way, and we are now looking for news on new nat gas wells or the Uinta Basin to launch us to the upside.

Thursday, June 5, 2008

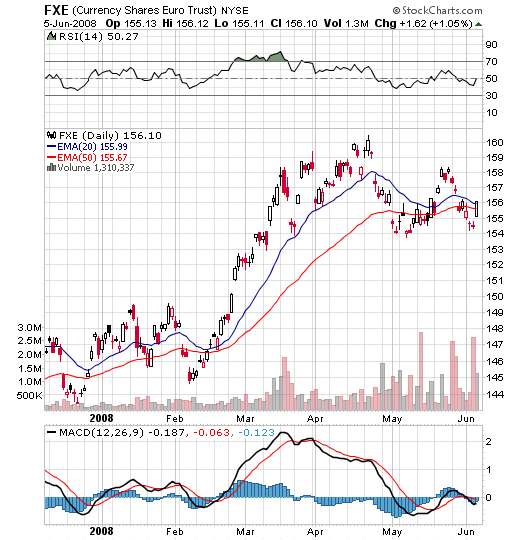

MXC PDO FPP Preparing To Squeeze As Oil Headed To New Highs On Another Round of Dollar Selling...

Oil has now completed a 50% retracement of its move from the $110 breakout level to the recent high of $135. After testing the $122.50 retracement level we saw an explosive +$5 move up in crude today on the heels of another round of dollar selling pushing the Euro back above $1.56. This move was triggered after ECB president Jean Claude-Trichet stated that the European Central Bank was prepared to raise interest rates next month which would again put new pressure on the dollar as higher interest rates overseas tend to push up demand for euros as global investors seek to lock in higher rates. Furthermore, looking at the chart of the FXE which tracks the EUR/USD we can see that there is a near perfect double bottom at the $1.54 level, and today seems to be the beginning of the next leg up which we firmly believe will take the Euro back to the $1.60 level thereby pushing crude back to new highs above $135. Moreover, note the strength in MXC PDO and FPP on the charts, as crude oils +$10 move off its highs only brought new buyers in creating nice consolidation patterns in all 3. All 3 are trading above their 10 day EMAs and we view this as a sign of strong accumulation here at these levels, and we expect short squeezes to commence in the very near future as shorts have now found themselves trapped in these low float energy stocks. Another round of momentum brought on by new highs in crude oil have potential to push all 3 above their recent 52 week highs. As such we have taken positions in both PDO and FPP at $18.60-18.70 and $5.02-5.07 respectively. While we would have liked to play MXC as well, the liquidity is a bit too light for our liking.

Tuesday, June 3, 2008

Sell Half ROYL Position, Let The Rest Ride...

After an enormous high volume run up in ROYL shares we are taking half our position off the table here at 10.80-10.90 in afterhours from our $5.17 entry. We feel it is only prudent to protect some of our profits, as momentum has found its way here and we need to lock in some of our 100% gains and begin looking for greener pasture. Technicals are clearly overbought now with an RSI just under 90 so we would like to see a nice pullback to possibly reposition ourselves. We still believe the stock should be valued much higher in the $15-20 range, and as such we continue to hold half our position for higher prices.

Monday, June 2, 2008

Stay 100% Long Royale Energy (ROYL): Initial Target Upped to $15-20 Based on Value of Uintah Basin Property...

For new ROYL longs please revisit last week's Wednesday May 28th blog for a complete recap of our bullish position on Royale Energy. For longs that are in with us from last week, well we are sitting pretty here as the stock has made a very significant breakout today on the strongest volume since 2005. While we would normally take profits here after a quick +60% pop from our entry, we are recommending holding all shares and are upping our initial target from $10 to the $15-20 range. We are basing our target on the significant value of their Uintah Basin property in Utah which has not only been validated by Anadarko's estimates of as much as 9 trillion cubic feet of nat gas on their 225,000 acres just south of Royale's, but has also just recently been validated by Whiting Petroleum's (WLL) $365M all cash acquisition of 11,534 net acres in the Uintah Basin from Chicago Energy Associates.

Here is a link to the PR put out by WLL after the close on friday which may explain the breakout in ROYL today:

http://biz.yahoo.com/prnews/080530/laf054.html?.v=98

Based on Whiting's $365M acquisition price which translates to $31,645 per net acre, it puts a value of approximately $475M on Royale's 15,000 net acres which are adjacent to WLL's newly acquired property. Now maybe my math is off, and maybe there is less natural gas in Royale's acreage so let's be ultra conservative and discount the value of Royale's property by 50% to $237.5M. Even after today's significant breakout, Royale's current market cap sits at a mere $65M! Which means anyway you slice it, Royale is extremely undervalued here and leaves room for enormous upside. Hence, based on the possible value of Royale's property, we are upping our initial target to $15-20 thereby giving ROYL a more reasonable yet still undervalued market cap of $118M -158M. Now as we have said before we spoke to the company a week or so ago, and they informed us that we may actually be hearing of the amount of reserves found in their Uintah Basin property this month which they said would be "very exciting news." Once this news arrives it will definitely give us more color on how much to value the property. As of now however, we highly recommend staying completely long ROYL shares till at least $15 as the company sits squarely in the crosshairs of an ongoing bull market in natural gas.

Here is a link to the PR put out by WLL after the close on friday which may explain the breakout in ROYL today:

http://biz.yahoo.com/prnews/080530/laf054.html?.v=98

Based on Whiting's $365M acquisition price which translates to $31,645 per net acre, it puts a value of approximately $475M on Royale's 15,000 net acres which are adjacent to WLL's newly acquired property. Now maybe my math is off, and maybe there is less natural gas in Royale's acreage so let's be ultra conservative and discount the value of Royale's property by 50% to $237.5M. Even after today's significant breakout, Royale's current market cap sits at a mere $65M! Which means anyway you slice it, Royale is extremely undervalued here and leaves room for enormous upside. Hence, based on the possible value of Royale's property, we are upping our initial target to $15-20 thereby giving ROYL a more reasonable yet still undervalued market cap of $118M -158M. Now as we have said before we spoke to the company a week or so ago, and they informed us that we may actually be hearing of the amount of reserves found in their Uintah Basin property this month which they said would be "very exciting news." Once this news arrives it will definitely give us more color on how much to value the property. As of now however, we highly recommend staying completely long ROYL shares till at least $15 as the company sits squarely in the crosshairs of an ongoing bull market in natural gas.

Thursday, May 29, 2008

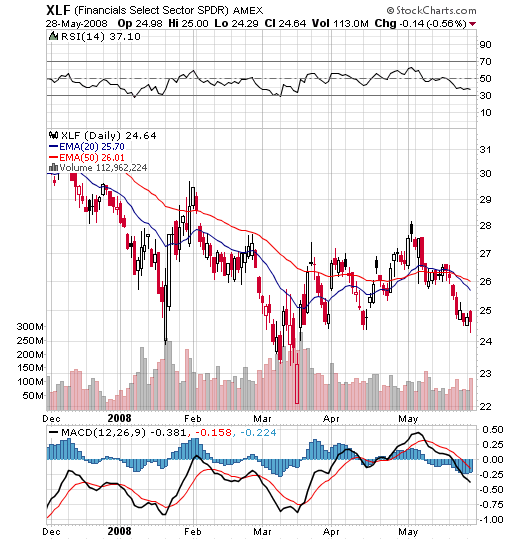

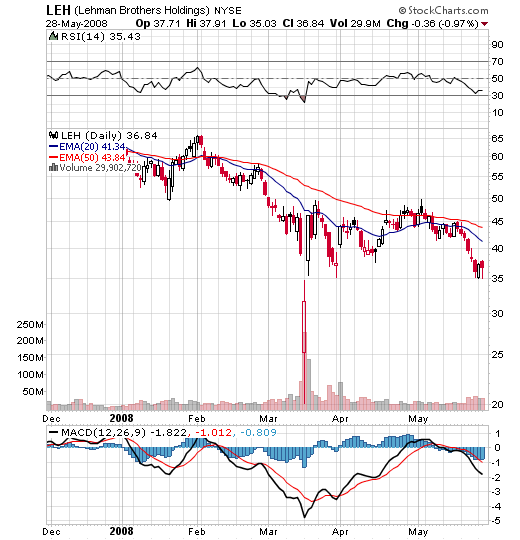

Price Action In Financials Signals Trouble Looming On The Horizon...

While most of us have been mesmerized by the price action in commodities, emerging markets and energy related plays over the past several weeks, it appears the financials have been making a rather stealthy yet alarming move to the downside. Looking at the 6 month chart of the XLF we notice that somehow we've managed to make our way back toward the lows set in March, and it appears that Lehman (LEH) has been looking ominously weaker than any other financial. Notably, David Einhorn of Greenlight Capital has been publicly parading the analysis behind his Lehman short position saying they are extremely undercapitalized and have essentially hidden $6.5 billion of CDOs on their balance sheet. Furthermore, credit default swaps on Lehman debt have begun rising dramatically over the past several weeks, going from 130 last month to just under 250 now. Merril debt has also spiked to 196. Taking into account these observations, a put position on the XLF as well as LEH seems like a good bet as something is definitely brewing within the financials yet again. If another round of credit woes surface the Fed may need to remain sidelined a bit longer than expected or we may actually begin to hear expectations of further rate cuts which would add further fuel to the commodity move. Would remain long Oil and Natural Gas, short XLF and LEH, short USD/EUR, and short the DIA here.

Wednesday, May 28, 2008

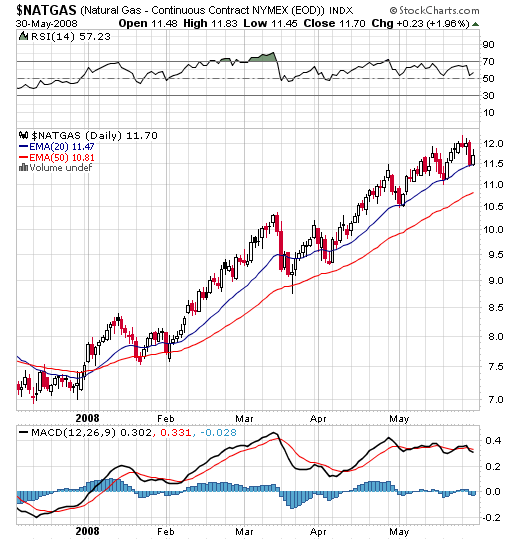

Buy Royale Energy (ROYL) As Natural Gas Prepares To Super Spike...

Watch for natural gas (currently at $11.90 per Mcf) to take out its December 2005 high of $15 in the next couple months in my opinion. As crude oil continues to gain traction and continues to make new highs it only puts added pressure on the price of natural gas as natural gas is widely known as the cleanest, most efficient energy source viable of replacing crude oil in the future. While natural gas is already being accumulated by large institutions preparing to play the energy of the future (notice the strong support at the 20 day EMA), the momentum crowd has yet to begin piling into the commodity as crude oil continues to maintain its luster as life of the commodity party. Sometime in the next couple of months, however, I believe natural gas prices will begin picking up in velocity and begin outpacing moves in crude oil. I expect natural gas prices to breach their December 2005 high and hit the $15-17 level and possibly higher. Now in terms of plays, to get the most bang for our buck an optimal play would be a small cap low float unhedged natural gas producer. This brought me to Royale Energy (ROYL). The company currently trades at $5.17 per share, has a mere $41M market cap, a 4.65M share float, is completely unhedged, and has been ramping natural gas production by putting new natural gas wells online. Not only that, they currently own 15,000 net acres in Utah's Uintah Basin where very large players such as Anadarko Petroleum are reporting that they have discovered enormous natural gas reserves. Anadarko which owns 225,000 acres in the Uintah Basin is estimating as much as 9 trillion cubic feet of potential reserves in the area just south of Royale's acreage. Royale has already begun exploring their acreage in the Uintah Basin as of late last year and has already successfully struck natural gas. This is an excerpt from last year's October press release:

"San Diego, November 27, 2007 – Royale Energy, Inc. (NASDAQ: ROYL)- Royale announces a new gas discovery and the successful completion and fracture stimulation of the V Canyon 20-1 well in the Uintah Basin.

On October 30th the completion rig was moved from the Ten Mile Canyon 22-1 well, to begin completion operations of the V Canyon 20-1. The well encountered multiple potentially productive zones including the Mesa Verde, the Sego, the Castlegate, the Mancos shale, the Dakota, the Brushy Basin, the Entrada and the Wingate. Out of a total of 60 feet of potentially productive Entrada, Royale selected the best 20 feet in the middle of the zone for perforation. This 20 foot section flowed gas naturally at an initial rate of 1.3 MMcf (million cubic feet) of gas per day and stabilized at 882 Mcf per day. Royale then decided to further stimulate by performing a fracture stimulation (“frac”) of this zone which increased the production capacity of the zone, resulting in an initial rate of 1.8 MMcf per day and stabilized flow rate of 1.04 MMcf of gas per day with higher tubing pressure. The well is currently being prepared for production and connection to the pipeline that runs

immediately north of the well."

Last week I spoke to the company, and they informed me that we may be hearing about the reserves found in the Uintah Basin in this upcoming month which they said would be "very exciting news." This news has potential to double the stock alone, and with additional wells coming online, as well as natural gas prices continuing to move higher, I expect Royale's share price trend to continue much higher, with eventual natural gas momentum taking this parabolically higher. The technicals look amazing as well as the stock is forming a bullish pennant after a high volume breakout from the $3 level, and is now finding strong support at the 10 day EMA. The stock is a buy here in the $5s with an initial target of +$10.

"San Diego, November 27, 2007 – Royale Energy, Inc. (NASDAQ: ROYL)- Royale announces a new gas discovery and the successful completion and fracture stimulation of the V Canyon 20-1 well in the Uintah Basin.

On October 30th the completion rig was moved from the Ten Mile Canyon 22-1 well, to begin completion operations of the V Canyon 20-1. The well encountered multiple potentially productive zones including the Mesa Verde, the Sego, the Castlegate, the Mancos shale, the Dakota, the Brushy Basin, the Entrada and the Wingate. Out of a total of 60 feet of potentially productive Entrada, Royale selected the best 20 feet in the middle of the zone for perforation. This 20 foot section flowed gas naturally at an initial rate of 1.3 MMcf (million cubic feet) of gas per day and stabilized at 882 Mcf per day. Royale then decided to further stimulate by performing a fracture stimulation (“frac”) of this zone which increased the production capacity of the zone, resulting in an initial rate of 1.8 MMcf per day and stabilized flow rate of 1.04 MMcf of gas per day with higher tubing pressure. The well is currently being prepared for production and connection to the pipeline that runs

immediately north of the well."

Last week I spoke to the company, and they informed me that we may be hearing about the reserves found in the Uintah Basin in this upcoming month which they said would be "very exciting news." This news has potential to double the stock alone, and with additional wells coming online, as well as natural gas prices continuing to move higher, I expect Royale's share price trend to continue much higher, with eventual natural gas momentum taking this parabolically higher. The technicals look amazing as well as the stock is forming a bullish pennant after a high volume breakout from the $3 level, and is now finding strong support at the 10 day EMA. The stock is a buy here in the $5s with an initial target of +$10.

Thursday, April 17, 2008

Get Long Boots & Coots International Well Control (WEL) @ $1.95 For Significant Growth In 2008...

I remember trading WEL for .30 back in 2003 when Saddam Hussein was on his way out of power and threatening to torch all his Oil wells. Back then Boots & Coots was a balance sheet disaster...tons of debt, hardly any cash, and paltry revenue mostly coming from their emergency Well Control business. However, things have changed remarkably at the Houston based company over the past few years. With the addition of several new business lines focused on servicing and maintaining onshore and offshore oil and gas rigs, revenue has grown significantly going from $29.5M in 2005, to $97M in 2006, to $105M in 2007. This dramatic growth is not only expected to continue this year but it is expected to ramp up a staggering 40% to $147M! In 2009 analysts are anticipating even further top line growth to $175M! Not bad for a company with a current market cap of $148M. Looking at earnings the story gets even better with EPS expected to more than double from 2007's .11 to .23 per share in 2008. This estimate may even appear to be somewhat conservative as last quarter the company guided for .02 and came it a whopping .08. However, assuming the company will earn the .23 analysts are estimating this year we are looking at a trailing P/E of a mere 8! And with analysts estimating .29 for 2009 the forward P/E shrinks even further to 6! Given the company's 40% revenue and 100% EPS growth projections we believe the market will begin accurately valuing the company very soon especially in light of the market's current focus on large cap Oil services names as well as the dramatic rise in spot Oil prices. We don't think it's far fetched for the market to reward WEL with a decent 20 times forward earnings multiple or $6/share given the company's growth figures. With Boots & Coots' worldwide presence (they do business in North America, South America, Africa, and the Middle East) we believe they are in a prime position to take advantage of the increased interest in maintaining highly valuable onshore and offshore oil and gas rigs. We recommend getting long shares here under $2 ahead of earnings after the close on May 5th as we expect another blowout quarter and expect the market to begin taking notice of Boots & Coots' significant growth trajectory.

Thursday, April 10, 2008

Get Short Intuitive Surgical (ISRG) @ $355 For Possible Double Top...

With ISRG now approaching its December 2007 high at $359.59, we like the risk/reward on a short position here at $355. On the charts we're looking for the possibility of a near perfect double top (see chart below) with a good 50 points downside as the 50% retracement of the move off the March lows at $255 to the April highs $359 gets us to $307. We will cover on any close above $360 as this would produce a vicious double top breakout on the charts. Hence, our risk is 5 points and our reward is ~50...we'll take it.

Wednesday, April 9, 2008

Oil: Next Stop $115-117, Euro To $1.61-1.62...

With Oil forming a perfect double bottom at $100 on the charts, and now taking out our previous high of ~$111 it is setting up for a ferocious double top breakout here which should take it to the $115-117 level. The commodity continues to look like a raging bull, bouncing off all expected support levels, and continuing to bust through major resistance levels one after another. We reiterate that funds from around the globe are finding it absolutely necessary to get long the commodity as an inflation hedge. The fundamental backdrop remains firmly intact with the dollar continuing to make new lows and we expect the euro to clear its $1.59 high shortly and head to the $1.61-1.62 level near term. This move should add further fuel to the commodity move. Remain long Oil, long Euro, short Equities near term.

Saturday, April 5, 2008

Part 1: Global Darwinian Forces May Produce Major Exogenous Event Blindsiding US Economy...

By all economic measures, the United States is clearly in a state of marked weakness. Economic growth is at or near zero, unemployment is rising, the banking system is in critical condition, housing prices continue to decline, the US consumer is up to its ears in debt, the dollar continues to make new lows versus every major currency, inflation shows no signs of abating, and the Fed is running around like a headless chicken literally doing everything it can to prevent the entire system from collapsing. This is not a subjective assessment, it is our grave reality. So what now? Where do we go from here?

Well the obvious answer would be to fix everything that appears to be broken, clean up inefficient systems, attempt to reinvigorate the economy, and ultimately rebuild confidence in the US financial system over time. However, what I fear most is that in this time of distress we may no longer have the luxury of time. I believe it is possible that one of the many emerging superpowers may make a play for global dominance in the near future. Yes, I know this is a bold statement, but let me explain. Over the past several decades the United States has clearly been the world's superpower. It has been the steam engine driving the global economy as continuous wealth creation here has driven demand for foreign goods thereby creating wealth and GDP growth overseas. We are clearly the largest consuming nation in the world, and most of our foreign counterparties have done everything they can to see that growth here continues as incremental gains in US GDP inevitably trickle down to their own economies. However, it appears now that the global economy has approached the point where our significance in the global growth equation has diminished. It appears as if our emerging market counterparties have grown to a level where collectively they are able to maintain global growth without the neccessity of US demand. Where is the evidence of this? The commodities market. We have virtually every major commodity (Gold, Oil, Coal, Grains, Corn) at or near nominal highs, with many now approaching their inflation-adjusted highs. What is most notable however is that these commodities are making this move with the United States literally on the brink of recession! How is this possible? How is it possible that Oil is near $110 per barrel with such weak US demand? How is it possible with the US near recession that global Oil demand is still greater than global Oil supply with Oil being pumped at maximum capacity? It is because of decoupling. The world no longer relies on the US as the primary engine of global growth anymore. This position has been taken over by the likes of China, India, and Brazil. While the US has been toiling with credit crises, a housing slump, and increasing debt loads, the emerging economies have grown into such a dominant state of hypergrowth that their only challenge is to make sure that growth does not get so excessive that it becomes unsustainable, and moreover that inflation remains contained. This dominant position, I'm afraid, may produce some sort of climactic consequence for the United States. Let me explain.

We as mere individuals, will never understand the desire to become a global superpower. This desire is something reserved for continents, nations, and unions as it is impossible for us as mere individuals to achieve such status. However, even though we may not have the capacity to understand this desire, we know that it exists. We know that every single day every sovereign nation is actively working or has the innate desire to become the strongest entity in the world. Why does this happen? What is the driving force behind this phenomenon? Well in my opinion it is driven by the underlying principle that the world lacks enough supply of natural resources to prolong the existence of every single nation over the long run. Over time, as the world begins to approach levels where natural resources are being fiercely competed over because of inadequate supplies and/or unusually high global demand at the margin, the strongest nations will attempt to force weaker nations into further weakness in the hope that this action may curtail overall demand and allow the strongest nations to accumulate necessary supplies at cheaper prices. It is Darwinism at its purest, and it is ultimately driven by the idea that while economic harmony may exist when the strongest parties are satisfied with the distribution of goods and resources, extreme competitive behavior will arise when those parties become dissatisfied with the allocation of resources, especially those resources necessary for independent survival. It is very much akin to the behavior of animals living in a jungle free from the so-called orders of society. When all animals including the strongest are fed and all so-called entities appear satisfied, harmony may exist because there is no need for competition as supplies of resources are adequate enough to meet the demands of all entities. However, if/when the strongest entities become dissatisfied with their levels of consumption, we will likely see an extreme uptick in competitive behavior as the idea of the natural order for satisfaction dictates that the strongest must be first to be completely satisfied. If/when this natural order appears to be imbalanced in that the strongest are not receiving adequate supplies, the strongest entities will likely seek to not only eliminate those entities which they believe will restore natural balance, but they will specifically seek to eliminate those who they believe will be easiest to eliminate (i.e. those entities who appear weakest). Make sense? Ok so what resource are we speaking of specifically when we speak of resources necessary for survival? We are speaking of crude Oil. Every single other commodity is secondary to crude oil in terms of necessity for survival. Gold, corn, wheat, coal, even steel are all secondary commodities. We don't need corn or even grain to survive, and coal and other fossil fuels are simply alternatives to the most important fossil fuel of all, crude oil. Without crude oil, factories would come to a stand still, refineries would be unable to produce gasoline, airplanes would be grounded, heating oil would be unable to be produced, and ultimately unemployment would skyrocket as productive inputs are unable to function and means of transportation become idle. It is the reason why there is literally no limit to how high the price of oil can go over the long run. Its significance as the world's primary energy source produces wars, wreaks havoc within the economic supply chain, and has the capacity to bring entire nations to its knees.

Part 2: The Consequence Of Weakness...coming soon