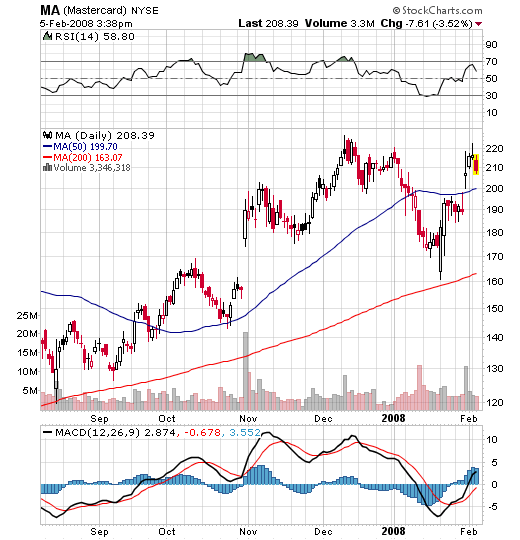

Mastercard has been on a great run over the past several months, and much of it has indeed been warranted based on the idea that during tough economic times, cash strapped consumers do in fact turn to plastic to finance much of their discretionary as well as non-discretionary items. And this is exactly what we have seen.... Mastercard's earnings have been stellar over the past several quarters on the heels of increased consumer transactions using plastic. Yet this rapid pace of increased credit transactions can not go on forever. Why? Because consumers have limited credit lines to finance items. Everyone has a credit limit, and with the increased rate of transactions we can safely say that over time consumers are getting closer and closer to their credit limits. We are also noting that we are in a slowing economy, and in a slowing economy, consumers are less likely to have the ability to pay down debt rapidly. Therefore, increased transactions will likely result in increased debt loads as consumers are less likely to service their debt obligations immediately. Moreover, we can say that the velocity of the move to approach their credit lines is very much a function of the pace of overall transactions. In other words, the more I use my Mastercard, the faster I get to my credit limit. Hence with an increase in the rate of overall transactions we can postulate a theory that consumers are getting closer and closer to approaching their credit limits, and therefore we may in fact begin to see the pace of consumer transactions decline. For you mathematicians out there, note that we are simply looking at the second derivative of consumer transactions. We are not saying that consumer transactions using plastic will decline, we are simply saying that the RATE of the increase in transactions using credit will begin to decline. This is the trend that I believe will begin to surface over the next few months. We will begin to see signs that consumers are getting tapped out in terms of using their credit lines to finance the purchase of goods. This will indeed take a toll on Mastercards earnings, and once the market is fully aware of this, I believe we will see a rapid selloff in the stock. It will be similar to the reaction we saw in Google....as institutions begin to realize that Mastercard's rate of growth is declining we will see a contraction in P/E, as well as a decrease in analyst earnings expectations which will result in a much lower stock price.

Also, taking a look at Mastercards institutional ownership we can see that the float is 85% owned by institutions which means that most of the moves in MAs stock will be dictated by institutional adjustments. Since insitutions are much smarter than the average joe, I believe that they are beginning to expect this trend and are in the process of slowly scaling out of MA here using the volume surge produced by last Thursdays earnings beat. We can see this on the 5 day chart as the stock has failed to close over the 220 level on multiple occasions now. The inability of the stock to breach $220 has also produced a possible double top at $220 on the 6 month chart. Given these observations, as well as my overall bearishness on the market, I believe MAs risk/reward profile warrants a bet to the short side here at $210....and we will make the 200 day MA at $163 our first target.

No comments:

Post a Comment